Macquarie Atlas Roads Group

.png)

MQA Details

Improved performance with rise in traffic: Macquarie Atlas Roads Group (ASX: MQA) reported that its 1H16 results entailed 6% growth in revenue and 4.2% rise in traffic owing to higher volumes and toll increases on Autoroutes Paris-Rhin-Rhone (APRR) and Dulles Greenway. 1H16 profit from operations has been up to $54.2 million against prior corresponding period’s $40.3 million. The group has announced for FY17 distribution guidance of 20 cents per share, which is up 11% on FY6. MQA earlier announced about the completion of sell down of Macquarie Group’s stake in MQA. About 53 million securities have been sold at $5.32 per security to a range of institutional investors. Macquarie interest in MQA post the sell-down is said to be about 11%. MQA also divested two of its six assets and is continuing to see traffic growth in the US.

.png)

APRR EBITDA and France GDP Growth (Source: Company Reports)

MQA delivered 19.8% returns during this year to date (as of September 27, 2016). We believe the stock has more momentum and accordingly, we maintain a “Hold” recommendation on this dividend yield stock at the current price of $4.98

MQA Daily Chart (Source: Thomson Reuters)

Vmoto Ltd

.png)

VMT Details

Weakness in 1H16 results but 2H16 expected to be stronger: Vmoto Ltd (ASX: VMT) reported for drop in revenue for 1H16 to $17.8 million from $24.9 million of 1H15 while net loss was $597,472 against 1H15 NPAT of $1 million. There has been a slow-down in sales of lower value electric two-wheel vehicles in Vietnam and Africa, which impacted the results to some extent. VMT clarified that local Chinese government restrictions have not been material to unit sales. On the other hand, the cash at bank is $4.6 million. The group has also formed a new subsidiary with PowerEagle in Shangai and the same is now operational. VMT has also commenced shipment for orders to a significant European supermarket group that has over 300 stores in Europe. VMT’s client LOOPShare Ltd had got successfully listed on TSX Venture Exchange in Canada and secured funding in July 2016. VMT has launched the marketing campaign “Ride Your Way” in Australia via online social media to drive traffic to Vmoto’s internet based online sales platform to offer electric vehicle products. Additionally, VMT has made the market entry, distribution and customer opportunities, for regions including North America, Netherlands, France, Mexico, Nepal, Thailand, Uruguay and Sri Lanka.

The group is expecting the second half of the year to be stronger than first half which was operationally a busy period. The stock has fallen 18.75% in last one month but rose 4% in last five days (as on September 27, 2016). We give a “Speculative Buy” recommendation on the stock at the current price of $0.13

VMT Daily Chart (Source: Thomson Reuters)

Nearmap Ltd

.png)

NEA Details

Strong FY16 performance: Nearmap Ltd (ASX: NEA) has delivered successfully on three key priorities for FY16 that entail accelerated growth in Australian business, foundations built for success in the US and technology leadership enhancement, and the revenue growth has been witnessed over the last four consecutive halves. The Australian business demonstrated about 38% growth in ACV portfolio while estimated lifetime portfolio value is of $338M. In fact, there has been a 63.6% year on year growth in subscription ACV values of top 10 Australian customers. For the US, closing ACV portfolio of US$1.5M with key customer wins from competitors was reported. NEA’s growth was based on disciplined cost management in H2 FY16 with expenses down on H1 FY16 while there was a 38% growth in receipts from customers in FY16. NEA’s business is well-funded with $12.2M of cash at year end. The group’s HyperCamera2 has gained attraction as the system will allow to capture, process and publish 3D models of what is on the ground which will add value to the customers who use these models in their planning, assessments and quoting. NEA earlier signed a significant new one-year subscription contract (annual value of $1.1 million) with an existing customer, which is one of Australia’s largest digital infrastructure companies.

.png)

Revenue Growth (Source: Company Reports)

Meanwhile, the stock has surged 51.3% this year to date (as of September 27, 2016). We give a “Buy” recommendation on the stock at the current price of $0.585

NEA Daily Chart (Source: Thomson Reuters)

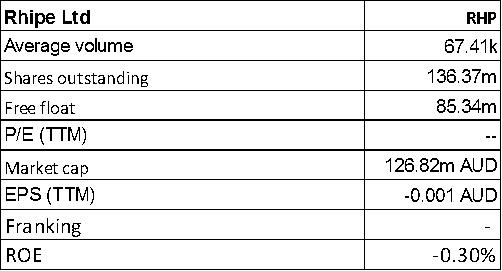

Rhipe Ltd

RHPDetails

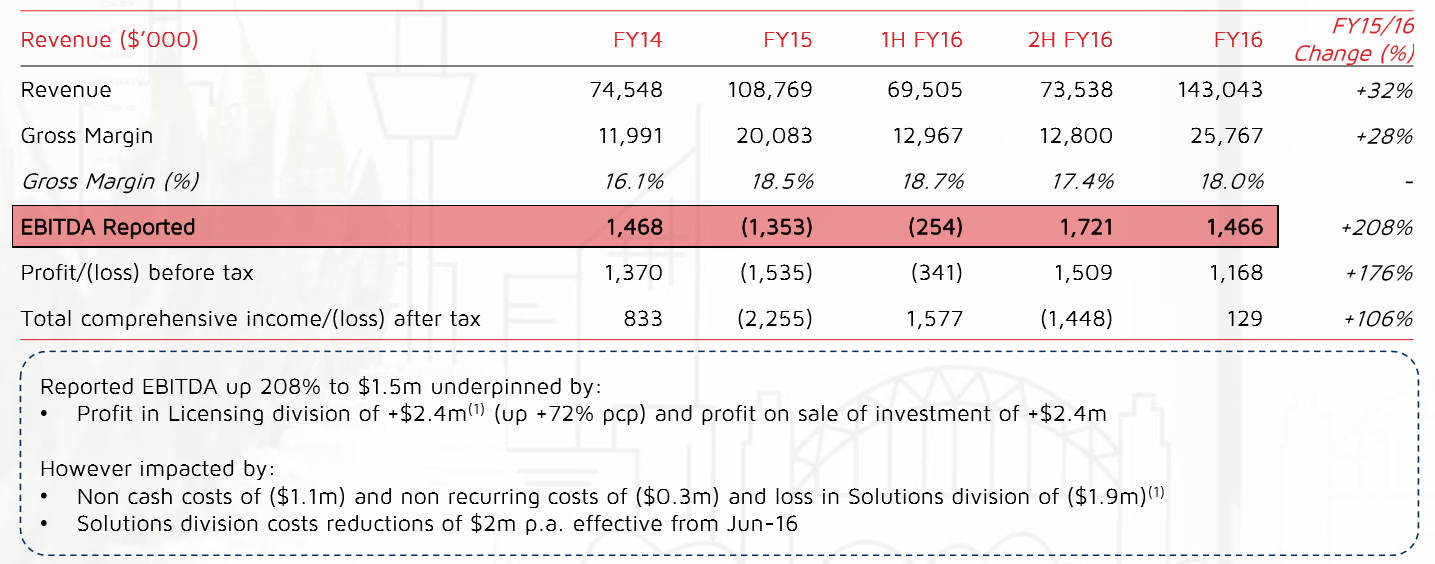

Top-line growth: Rhipe Ltd (ASX: RHP) stock fell over 9.71% in the last one month (as of September 27, 2016). On the other hand, RHP has won three Microsoft Australia Partner Awards and has been the only partner to win the awards this year. The group’s revenue has been up 32% to $143 million while licensing sales have grown 38%. Further, the gross margin has been up while the underlying licensing EBITDA is up 40% to $7.1 million. The group’s investments have been strong. For instance, RHP witnessed SEA revenue growth of 87% while LSP has been profitable at 30 June 2016 and LiveTiles is partially monetised with profit of $2.4m. The group is debt free and expects to have FY17 reported EBITDA of $5 million.

Financial Performance (Source: Company Reports)

We believe the correction in the stock placed them at reasonable levels. We give a “Speculative Buy” recommendation on the stock at the current price of $0.95

RHP Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.