Bellamy's Australia Ltd

.png)

BAL Details

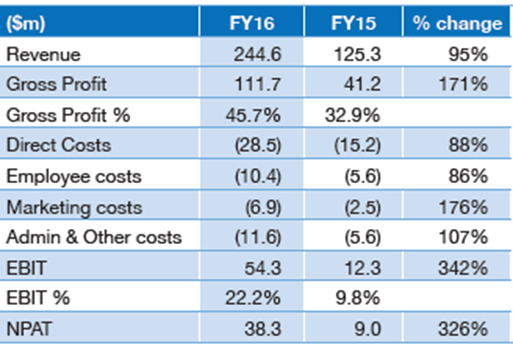

Very strong gross profit in FY 16: Bellamy's Australia Ltd (ASX: BAL) has reported an EBIT growth of 342% to $54.3m in FY 16, while the revenue grew 95% to $245m. In fact, China’s revenues surged 331% ending investor’s concerns of the group’s potential performance in the region. The revenue grew on the back of better infant formula production, Australian price increase for the infant formula range in December 2015 and high volumes’ direct to China following activation of China online reseller channels.

FY 16 Financial Performance (Source: Company Reports)

Moreover, BAL has strong cost management driven by the growth in the business infrastructure as the head count has increased by 50%. BAL would enhance the manufacturing volume in FY17 which will increase the inventory build for growth in existing and new markets. In addition, BAL would benefit from new Chinese regulations, which would limit registered factories in China and offshore to producing three brands and each brand to three products. BAL stock rose 13.2% in the last six months (as of September 23, 2016), and we give a “Hold” recommendation on the stock at the current price of $12.99

.PNG)

BAL Daily Chart (Source: Thomson Reuters)

Catapult Group International Ltd

.png)

CAT Details

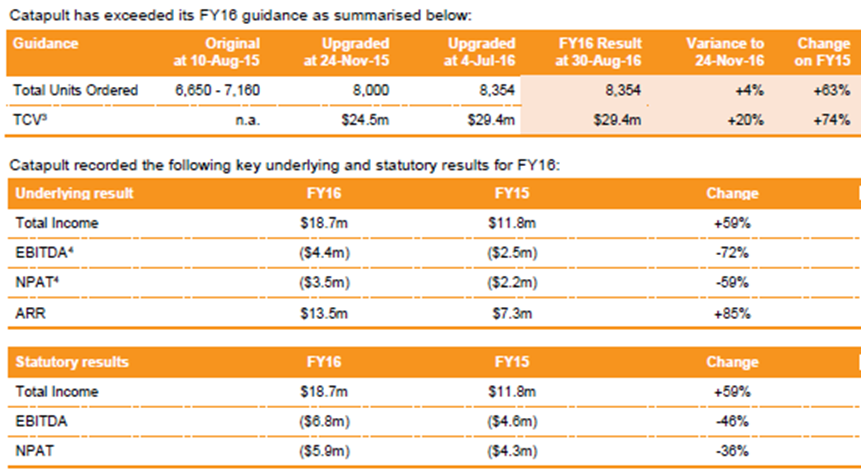

Weak bottom line in FY 16: Catapult Group International Ltd (ASX: CAT) has exceeded guidance for the total units ordered which is up 63% to 8,354 in FY 16 and the total contract value (TCV) which is up 74% to $29.4m.

FY 16 Financial Performance (Source: Company Reports)

However, the underlying NPAT fell 59% to $3.5million. Moreover, in FY 17, CAT expects to accelerate transition to positive EBITDA and free cash flow after the acquisition of XOS. With this move, the group is targeting for cross-sell opportunities in XOS’ current client base and a market opportunity after the acquisition of PLAYERTEK.

Meanwhile, CAT stock rose over 75.27% in the last six months (as of September 23, 2016) placing the stock at higher levels. We believe that the stock is “Expensive” at the current price of $3.57

CAT Daily Chart (Source: Thomson Reuters)

Sealink Travel Group Ltd

.png)

SLK Details

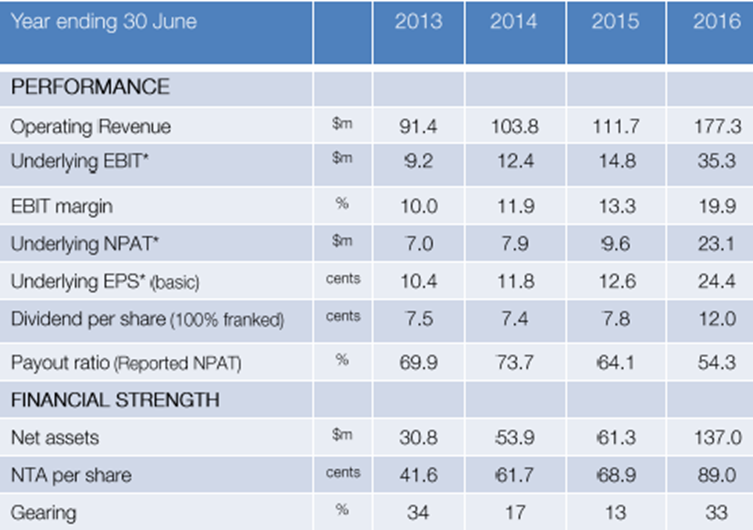

Strong growth in underlying NPAT:Sealink Travel Group Ltd (ASX: SLK) reported a 141% increase in underlying NPAT from $9.6 million to $23.1 million in FY 16 before the expenses related to acquisitions. The growth is due to the acquisition of the Gladstone and South East Queensland and organic growth in pre-acquisition businesses. The underlying basic earnings per share reached 24.4 cents which is 94% increase against 2015 earnings per share of 12.6 cents.

FY 16 Financial Performance (Source: Company Reports)

The revenue grew by 5.4% from $111.7m to $117.8m for the pre-acquisition business units, driven by higher tourism sales for Captain Cook Cruises NSW, growth in SeaLink’s Kangaroo Island ferry and tour operations, and new ferry route services and increased Hop-On Hop-Off sales on Sydney Harbour.

Moreover, SLK expects EBIT from its Gladstone operations to be approximately $2.0m lower in FY 2017 than FY 2016 due to the continuing transition from construction to operational phase of the LNG plants, which is expected to be completed by March 2017. We give a “Hold” recommendation on the stock at the current price of $4.45

SLK Daily Chart (Source: Thomson Reuters)

JB Hi Fi Limited

.png)

JBH Details

Finally acquired The Good Guys: JB Hi-Fi Limited (ASX: JBH) recently completed the dispatch of the retail offer booklet (1 for 6.60 pro rata accelerated renounceable entitlement offer at $26.20 per new share) and has also acquired 100% of The Good Guys for the total cash consideration of $870 million. The acquisition would boost the group’s presence in the home appliances market and is expected to deliver net synergies of $15 - 20 million per annum to the combined business after a three-year integration period, excluding one-off implementation costs.

.png)

Overview of the Transaction (Source: Company Reports)

Meanwhile, JBH stock rose over 21.98% in the last three months (as of September 23, 2016), and we believe that there is still some momentum left in the stock. Based on the foregoing, we give a “Hold” recommendation on the stock at the current price of $29.31

.PNG)

JBH Daily Chart (Source: Thomson Reuters)

Bapcor Ltd

.png)

BAP Details

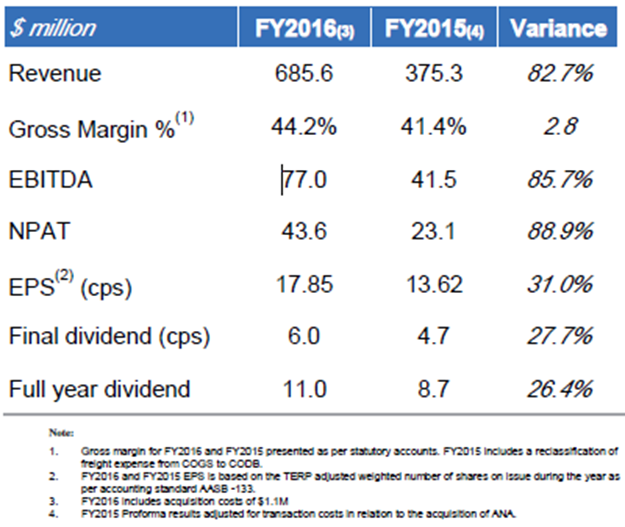

ANA acquisition contributed significantly to the topline growth in FY 16: Bapcor Ltd (ASX: BAP) reported an 82.7% increase in revenue to $685.6 million in FY 16 in which ANA acquisition contributed 67.9%, and 88.9% growth in the NPAT (net profit after tax) of $43.6 million. Moreover, BAP expects NPAT to increase in the range of 25%-30% in FY17 from FY16.

FY 16 Financial Performance (Source: Company Reports)

However, BAP is reviewing its car servicing business (part of the Retail segment) to determine its future. The Specialist Wholesale division has faced challenges for fully passing on costs to the market, which led to lower margins. Moreover, BAP stock rose over 36.98% in the last six months (as of September 23, 2016), placing the stock trading at a high P/E while dividend yield is also low. We give an “Expensive” recommendation on the stock at the current price of $6.22

BAP Daily Chart (Source: Thomson Reuters)

Credit Corp Group Ltd

.png)

CCP Details

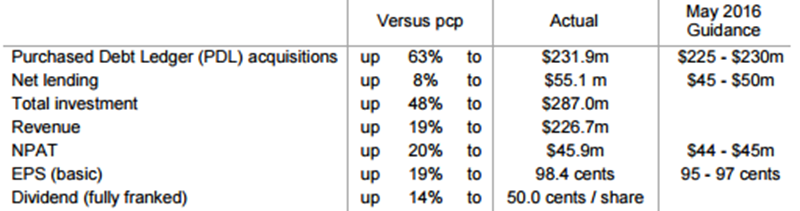

Beaten the estimates: Credit Corp Group Limited (ASX: CCP) has acquired National Credit Management Limited (NCML) from Thorn Group Limited for $22.6 million subject to completion adjustments. The acquisition necessitates upgrade to PDL purchasing guidance. CCP earlier reported a 19% growth in revenue in FY16 due to a strong increase in PDL collections, combined with significant growth in the loan book. Moreover, CCP has delivered a 20 per cent increase in NPAT to $45.9m beating the guidance of NPAT to be in the range of $44 - $45m mainly due to the growth from core domestic debt buying and significantly higher earnings from the consumer lending business. The earnings per share grew 19% to 98.4 cents beating the estimate of 95 - 97 cents. CCP has done an investment of $287.0 million in FY 16 to sustain growth.

FY 16 Financial Performance (Source: Company Reports)

Additionally, CCP has given a positive outlook for all the businesses and forecasts FY2017 NPAT growth guidance of 13 to 18 per cent. As a result, CCP stock already rose over 79.92% in the last six months (as of September 23, 2016), the trading at a high P/E against its peers. Hence, we give an “Expensive” recommendation on the stock at the current price of $18.07

CCP Daily Chart (Source: Thomson Reuters)

Aconex Ltd

.png)

ACX Details

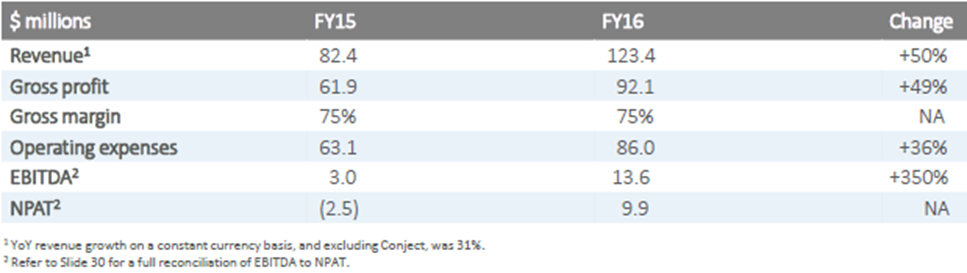

Key acquisitions in FY 16: Aconex Ltd (ASX: ACX) has reported a 50% growth in the total revenue to $123.4 million in FY 16 due to the strong organic growth plus the acquisition of Conject. ACX posted net profit after tax (NPAT) from core operations in FY16 of $9.9 million, compared with a net loss of $2.5 million for FY15. Moreover, ACX completed three acquisitions in FY 16, namely Worksite for cost and schedule project controls, the CIMIC Group’s INCITE Keystone collaboration platform and Conject for consolidated global leadership and scale.

FY 16 Financial Performance (Source: Company Reports)

On the other hand, ACX stock fell over 9.42% in the last three months (as of September 23, 2016) as investors along with insiders were booking their profits in the stock. Despite this fall, ACX stock is trading at an unreasonable P/E and accordingly, we give an “Expensive” recommendation on the stock at the current price of $6.52

ACX Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.