Healthscope Ltd

.png)

HSO Details

Hospital expansion program is on track:Healthscope Ltd (ASX: HSO) reported a 18.9% growth in statutory NPAT to $182.8 million in FY 16 and 6.2% growth in the revenue to $2,291 million as compared to the corresponding period 2015. This is due to the robust performance of the Hospitals and New Zealand Pathology divisions and a reduction in interest expense as a result of the post-IPO capital structure.

.png)

Financial Performance (Source: Company Reports)

Moreover, the group’s hospital expansion program is said to be on track and the three major brownfield projects are completed in 2HFY16. Given this performance, HSO stock rallied over 18.8% in the last six months (as of September 05, 2016), and we believe there is more upside left in the stock. Accordingly, we give a “Hold” recommendation on the stock at the current price of $3.01

HSO Daily Chart (Source: Thomson Reuters)

Insurance Australia Group Ltd

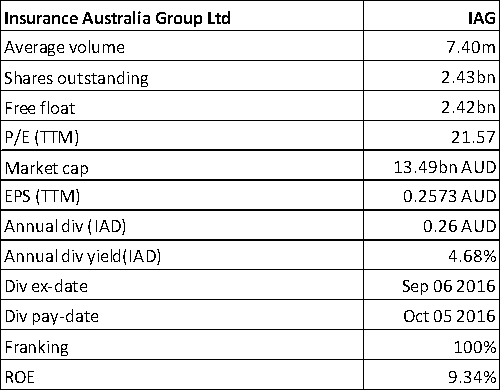

IAG Details

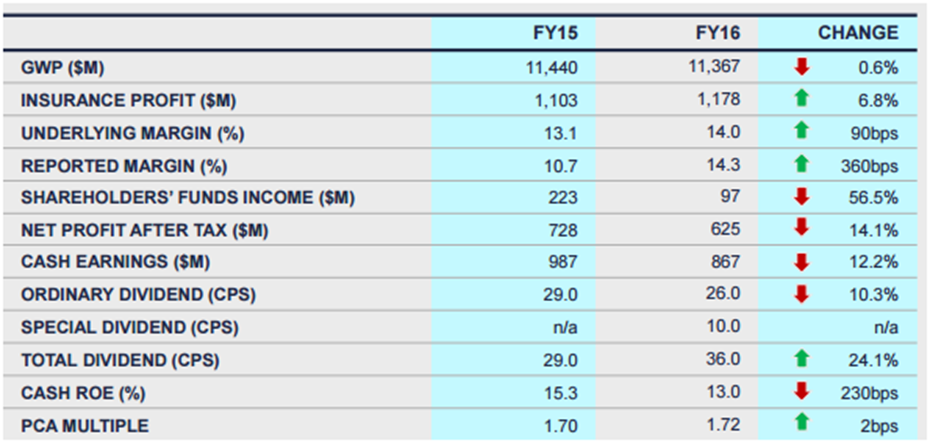

Ongoing buy back initiatives supporting the stock: Insurance Australia Group Ltd (ASX: IAG) reported a 14.1% fall in the net profit after tax to $625 million for fiscal year of 2016. Moreover, IAG’s reported margin guidance for FY17 is 12.5-14.5%; and for FY17, IAG expects the GWP will be relatively flat. As a result, the stock fell over 6% in the last four weeks (as of September 05, 2016). The stock traded ex-dividend on September 06, 2016.

FY 16 Financial Performance (Source: Company Reports)

On the other hand, the insurance profit grew 6.8% to $1.18 billion in FY15 and the group delivered a modest GWP contraction and a reported margin of 14.3%.

IAG is even leveraging the subdued levels in the stock via $300 million off-market share buy-back as part of the capital management programme which is expected to be completed in mid-October 2016, and support the stock at lower levels. Having a decent dividend yield, we give a “Hold” recommendation on the stock at the current price of $5.45

IAG Daily Chart (Source: Thomson Reuters)

ALS Ltd

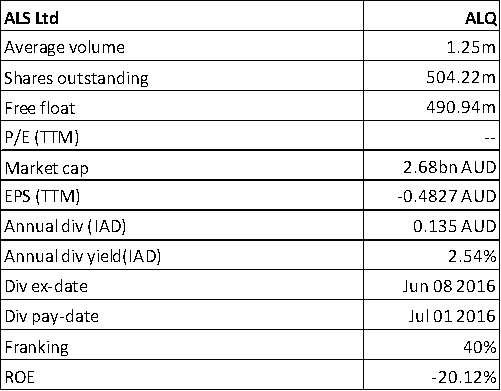

ALQDetails

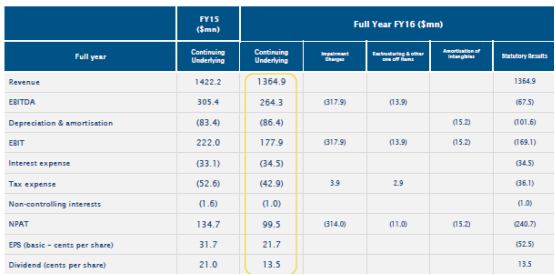

First half of 2017 profit is expected to be subdued: ALS Ltd (ASX: ALQ) reported an underlying net profit after tax of $99.5 million in FY 16, which is 27% lower due to the ongoing commodity price uncertainty. The statutory net loss after tax is $240.7 million for the FY 16 primarily due to non-cash impairment charges of $314 million after tax against ALQ’s oil and gas investments.

FY 16 Financial Performance (Source: Company Reports)

The revenue from continuing operations is $1.365 billion, slightly down from the $1.4 billion in FY 15. Moreover, ALQ is expecting 1H FY17 underlying after tax profit to be in the range of $50 to $55 million, as compared with $61.9 million in the 1H FY16. We give an “Expensive” recommendation on the stock at the current price of $5.43

ALQ Daily Chart (Source: Thomson Reuters)

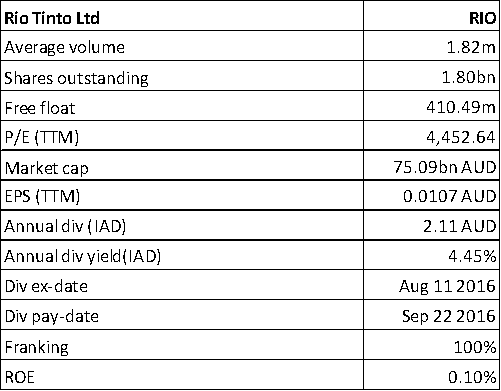

Rio Tinto Limited

RIO Details

Maintaining EBITDA margins:Rio Tinto Limited (ASX: RIO) has completed the sale of Mount Pleasant thermal coal assets to MACH Energy Australia Pty Ltd for US220.7 million and royalties. The company had reported consolidated sales revenues of $15.5 billion in 1H 2016 which is $2.5 billion lower than the 1H 2015 due to the decline in commodity prices. RIO has focused on cost reduction, and was able to reduce costs by $0.6 billion and still maintained a 33% EBITDA margin in 1H 2016.

The group has generated net cash from operating activities of $3.2 billion and reported underlying earnings of $1.6 billion. Moreover, RIO has delivered strong operational performances in iron ore, bauxite and aluminium, with all key commodities on track to meet full year guidance. We remain bullish on Rio and give a “Buy” recommendation at the current price of $48.53

RIO Daily Chart (Source: Thomson Reuters)

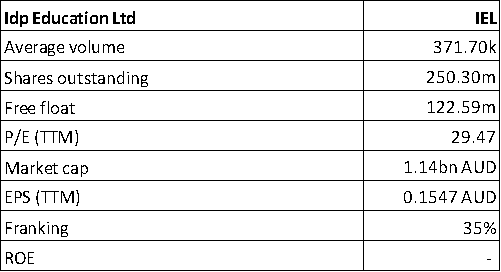

IDP Education Ltd

IELDetails

Exceeded the FY16 Prospectus Forecasts:IDP Education Ltd (ASX: IEL) reported the total revenue growth of 17% to $361.6 million in FY 16, while Net profit after tax (NPAT) grew 32% to $39.9 million as compared to the FY15 pro-forma. In FY 16, IEL has exceeded the forecast with EBIT 6.0% ahead of forecast and NPAT 12% above IEL’s prospectus forecast.

Meanwhile, the stock rose 11.59% in the last six months (as of September 05, 2016), placing it at a very high P/E. We believe that the stock is “Expensive” at the current price of $4.38

IEL Daily Chart (Source: Thomson Reuters)

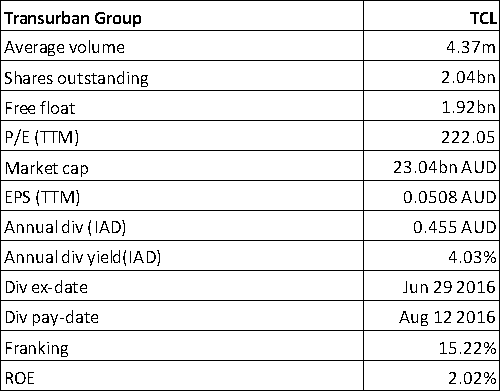

Transurban Group

TCL Details

Concerns over the debt:Transurban Group (ASX: TCL) reported a proportional toll revenue growth of 17.5% to $1,946 million in FY 16 and the average daily traffic (ADT) grew by 8.0%. Moreover, TCL has $9 billion of development projects to improve customers’ trips in Melbourne, Sydney, Brisbane and Greater Washington Area. In FY 16, TCL has distributed dividend of 45.5 cents per security; and for FY17, TCL has given the distribution guidance of 50.5 cps, which is an 11.0% increase on the FY16 distribution.

On the flip side, the group’s assets need to be returned to the government, which could impact the group’s value. TCL has a high debt of over $12 billion. We give an “Expensive” recommendation on the stock at the current price of $11.02

TCL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.